Tesla Stock Has Many Risks. EV Credits Isn’t One of Them.

Tesla bears need to stop harping on regulatory credit sales. The oft-repeated refrain is that Tesla isn’t profitable without credit sales. There are plenty of reasons bears can avoid Tesla stock, but credits Tesla earns, and then sells for cash to other auto makers, for producing more than its shares of zero emission vehicles isn’t one of them.

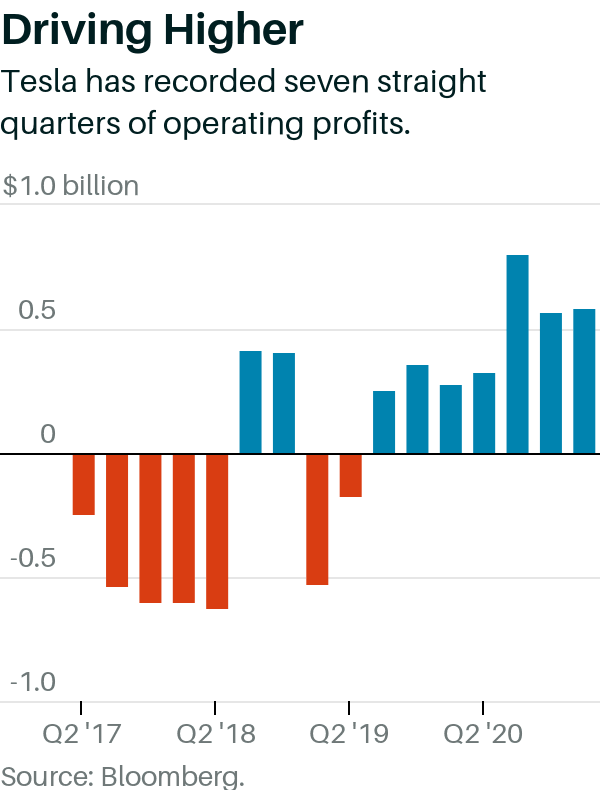

Tesla (ticker: TSLA) sold more than $500 million in regulatory credits in the first quarter and generated just under $600 million in operating profit. Excluding the credits, Tesla only eked out a small operating profit.

But saying Tesla isn’t profitable without regulatory credits is falling victim to the fallacy of the predetermined outcome. It’s like saying the New York Jets lost a football game because of a bad call in the first quarter. There are many reasons the Jets lose and a refereeing mistakes aren’t one of them.

To drive the analogy further, any Jets game would be totally different if the ref didn’t mess up. A penalty not called, or called, changes each subsequent play in unknown ways. If Tesla didn’t have regulatory credits to sell, the company would have to raise prices or cut costs or do something else to make money. The company would adapt to the situation.

Raising prices could be a way to go, but higher prices, of course, have their own impact, potentially reducing demand. Tesla still managed to grow sales even after the company lost its $7,500 U.S. federal tax credit. That isn’t available to Tesla buyers any longer because Tesla has sold too many EVs to qualify.

Tesla lost that federal credit at the end of 2019. It was effectively a $7,500 price increase in the U.S. on Jan. 1, 2020. Tesla sales in the U.S. grew 20% this past year, hitting $15.2 billion, up from $12.7 billion in 2019.

There is one other–rather large–point about regulatory credits. They aren’t going away. If anything, they will increase. Government support might morph from what Tesla sells today into new purchase tax credits or something else, but governments in China and the U.S. are looking to increase the number of EVs sold.

Refusing to deduct credit sales from operating income doesn’t make an investor a Tesla devotee. There are plenty of reasons people can choose to avoid the stock. Valuation being chief among them. Tesla is the world’s most valuable auto maker by a factor of roughly three even though it makes a fraction of the cars that Toyota Motor(TM), the second most valuable car company, does.

Valuation is a stale reason to dislike the stock. People have been complaining about valuation for a long time. Investors can also decide that competition is ramping higher or that full self-driving technology will take longer to develop than Tesla currently believes and suggests. Autonomous driving isn’t easy. Elon Musk calls it the company’s hardest challenge and its biggest potential value creator.

There is something in Tesla stock for full self-driving technology. How much is hard to say. Morgan Stanley analyst Adam Jonas values Tesla mobility and network services business opportunities at roughly $330 a share.

Those include software sales and robotaxis–both businesses are dependent on autonomous driving technology. His value is almost half of Tesla’s current stock price. Although Jonas’ Tesla target is $900 a share, making those business closer to one-third of the value he sees in the company.

Autonomous hiccups, valuation and competition should be enough reason to avoid the stock. Just stop saying the company doesn’t make money without regulatory credits.

Tesla shares are down about 2% year to date, trailing behind comparable gains of the S&P 500 and Dow Jones Industrial Average. Investors aren’t worried about the credit conundrum. They are waiting for quarterly operating profits to set new highs. When, and if, it does, they won’t care about the composition of the operating profit .